Monthly Trends

Monthly TrendsMeasures to contain the spread of the coronavirus in the Middle East were amped up in March, but did little to limit the damage done to the region's hotel industry, which was simultaneously thumped by an oil price war between Saudi Arabia and Russia, which required international intervention.

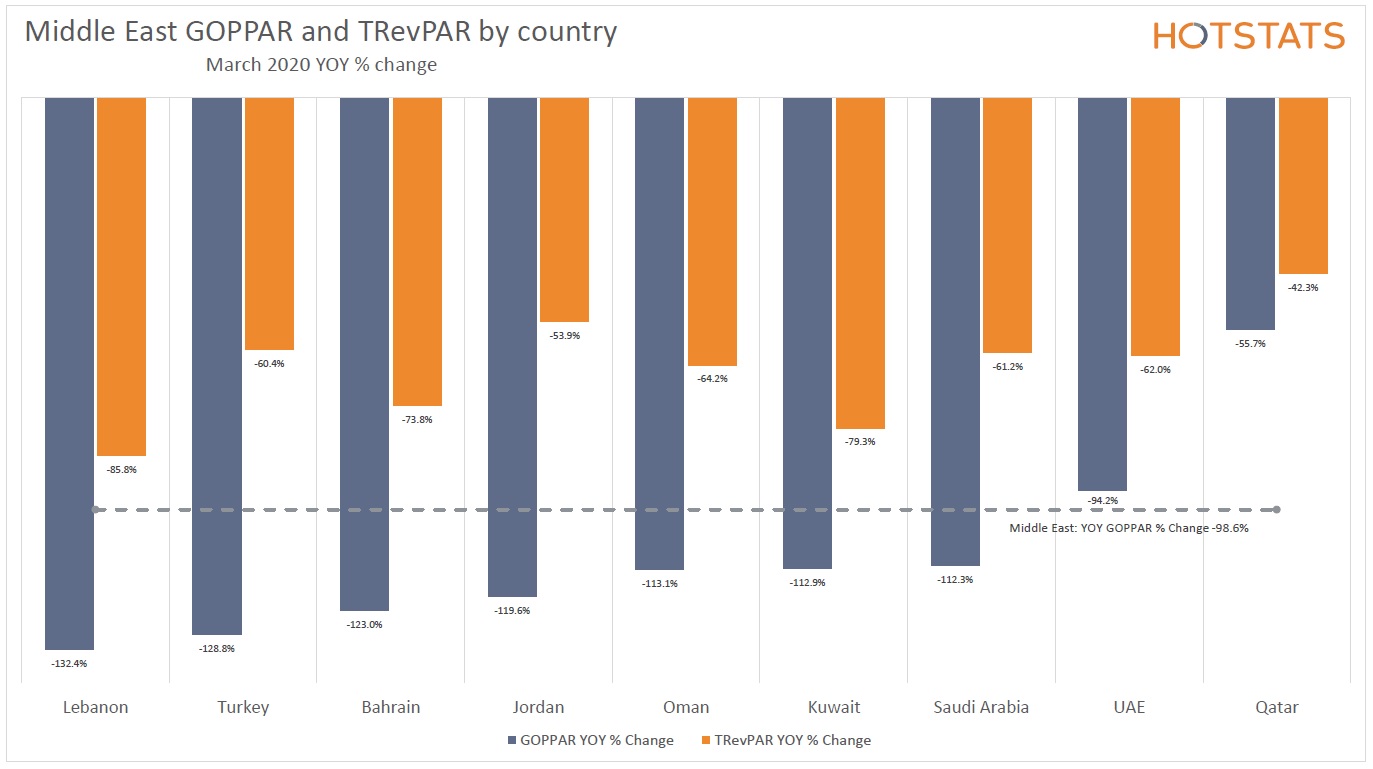

The combination reflected in the bleak profitability results recorded in the region in March. GOPPAR fell by a record 98.8% year-over-year, just about breaking even at $1.12.

Occupancy in March plummeted by 41.3 percentage points YOY to 34.6%, its lowest level since HotStats started tracking the region’s data. Average rate, which has been decreasing YOY consistently since June 2019, furthered its downward trend and recorded an 18.3% drop compared to March 2019. Consequently, RevPAR fell by 62.8% YOY. Declines across all other revenue centres resulted in a 61.7% YOY decrease in TRevPAR.

Trying to cope with the mammoth top-line contraction, hoteliers in the Middle East flexed costs to achieve a 27.0% YOY reduction in overheads and cut labour costs by 25.8% YOY. However, the efforts were not enough to sustain the region’s profit margin, which placed 39.5 percentage points below that of March 2019 at 1.5%.

The outbreak of COVID-19, combined with the oil price war, resulted in the worst Q1 performance ever recorded by HotStats in the Middle East in terms of profitability, as the 36.5% decline in GOPPAR was even greater than the 36.0% fall recorded in Q1 of 2011, amid the instability of the Arab Spring.

Hotels in Dubai started recording a profitability slump as early as February 2020, as GOPPAR decreased by 20.2% compared to the same month of the previous year. In March, the proliferation of lockdowns and travel bans across its visitor source markets in Europe, Asia, the Middle East and the United States deepened the performance slump, resulting in GOPPAR in the month placing 95.5% below that of the same period in 2019.

The severe contraction in demand, coupled with a pre-existing problem of oversupply, resulted in a 49.9-percentage-point YOY drop in occupancy in March, the largest drop ever recorded for Dubai in the HotStats database. Moreover, March marked the 35th consecutive month of YOY average rate drop, in this case, by 22.6%. As a result, RevPAR recorded a 67.0% YOY decrease. Total F&B revenue fell by 64.4% on a per-available-room basis, and with all other revenue streams dwindling, too, TRevPAR plummeted by 64.4% YOY.

Overhead costs per available room were slashed by 28.3% YOY due to falling expenses across all the undistributed departments. On this same line, total labour costs dropped by 31.1% YOY, led by a 32.8% payroll reduction in the F&B department and a 32.4% fall in Rooms. Nevertheless, profit conversion of total revenue fell by 39.3 percentage points compared to March 2019 to 5.7%.

Profit & Loss Performance Indicators – Dubai (in USD)

| KPI | March 2020 v. March 2019 | Q1 2020 v. Q1 2019 |

| RevPAR | -67.0% to $62.40 | -28.8% to $140.49 |

| TRevPAR | -64.4% to $113.76 | -28.0% to $233.97 |

| Labour Costs PAR | -31.1% to $50.43 | -19.5% to $61.70 |

| GOPPAR | -95.5% to $6.49 | -36.9% to $90.90 |

The first confirmed case of coronavirus in Qatar was recorded on February 27th, prompting authorities to take protective measures in early March. On March 9th, Qatar issued a travel ban on 15 countries, which was expanded five days later to include Germany, Spain and France. As a consequence, hotels in Doha recorded a 55.7% GOPPAR contraction in March compared to the same month of 2019. This result is in stark contrast to the marked profit-per-available room growth recorded in the first two months of the year, up 42.1% YOY in January and 24.5% YOY in February.

Average rate in Doha remained stable in March, recording a small downtick of 1.8% compared to the previous year. Therefore, with a 20-percentage-point YOY decrease, occupancy was the driving force behind the 27.4% YOY plunge in RevPAR, the first YOY fall recorded for this metric since May 2019. A further 53.7% YOY decline in F&B RevPAR resulted in a 42.3% YOY contraction of TRevPAR.

Efforts to flex expenses resulted in a 25.8% YOY decline in overheads and a further 20.4% YOY drop in total hotel labour costs per available room. And even though this was not enough to avoid profit erosion entirely, the loss in profit margin was minimal compared to the Middle East average. Thus, profit margin in Doha fell by 8.5 percentage points in March to 28.1%

Profit & Loss Performance Indicators – Doha (in USD)

| KPI | March 2020 v. March 2019 | Q1 2020 v. Q1 2019 |

| RevPAR | -27.4% to $78.14 | -6.8% to $92.42 |

| TRevPAR | -42.3% to $162.00 | -11.9% to $223.04 |

| Labour Costs PAR | -20.4% to $53.38 | -6.4% to $63.23 |

| GOPPAR | -55.7% to $45.57 | -5.9% to $76.32 |